When the economy weakens, a common anecdotal indicator is that home service professionals – plumbers, roofers, handymen, remodelers – start hustling harder for work. Homeowners tend to delay big projects (like roof replacements or bathroom remodels) when times are tough, so contractors respond by advertising deals and quick service to fill their schedules. The question is, how does this look in 2024–2025? Is the U.S. in a recession now, and if so, where are these trends most pronounced? Below we explore recent data on the home improvement market, focusing on pricing, availability, and marketing behaviors of home service pros as economic signals.

Economic Slowdown and Home Improvement Activity

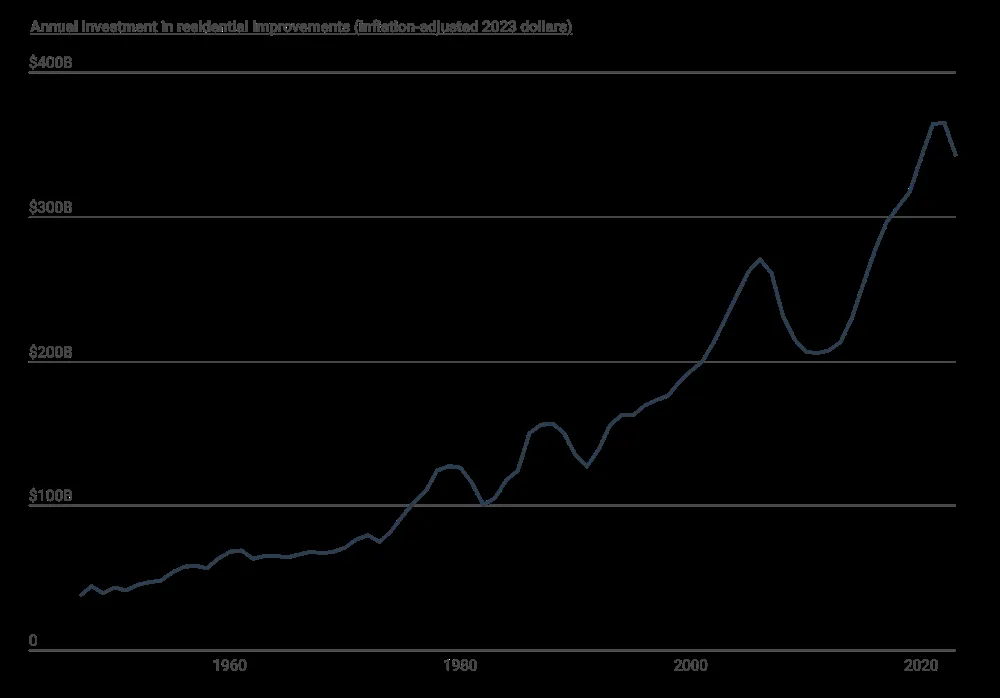

Annual U.S. investment in home improvements (inflation-adjusted dollars) surged during the pandemic boom, then plateaued in 2022 and declined in 2023, reflecting a cooler economy.* Home renovation spending typically falls during economic downturns , and indeed 2023 saw a pullback : the number of home improvement loans dropped from about 745,000 in 2022 to 565,000 in 2023. This reversal came after a decade of growth and a pandemic-era spike. It was triggered by rising interest rates, high inflation, and a slump in home sales , which sapped homeowners’ willingness to invest in upgrades. As one expert noted in mid-2023, “spending on home renovations is expected to slow this year” due to declining home sales and economic uncertainty. It’s important to clarify that the broader U.S. economy has not officially entered a recession as of late 2024/early 2025. Economists largely believe a formal recession will be avoided , though growth has been below potential and fraught with uncertainty. Instead of a crash, the home improvement market experienced a modest correction from its pandemic highs. Total home project spending dropped ~12% in 2024, reflecting the squeeze on household budgets. However, this dip is widely seen as temporary; industry forecasts predict mild growth returning by 2025 as financial conditions stabilize. In other words, the home improvement sector cooled significantly (akin to a recession for contractors) but is poised for a rebound , assuming the broader economy continues its slow improvement.

Signs of Slower Demand: Pricing and Availability

When homeowners delay remodels and non-essential repairs , home service pros often step up their game to win the limited jobs available. In practice, this means contractors market more aggressively and offer incentives to attract business. During the 2020–2021 boom, many tradespeople were so swamped with work that they could pick and choose jobs – some were booked for months and raised prices with impunity. Now, in a cooler market, they are generally more willing to negotiate and accommodate customers. For example, a custom carpenter in North Carolina saw his backlog shrink from a 90–160 day wait during the boom to around 30 days of work booked out once demand slowed in 2022 . Likewise, a handyman franchise owner in Massachusetts said he’s normally booked 3–4 weeks in advance, but recently that lead time fell to 2–3 weeks , as clients became more cost-conscious and opted for only small fixes. These shorter wait times signal that contractors have more availability now than in the recent past, making them eager to schedule new jobs. Home professionals are also pivoting their sales strategies . When big projects dry up, many shift focus to smaller or more affordable services – essentially meeting customers where their tighter budgets are. The Charlotte carpenter above started selling “ kitchen face-lifts ” (replacing cabinet fronts and repainting instead of full renovations) to give homeowners a refresh at a fraction of the cost of a new kitchen. This kind of value offering helps entice clients who might otherwise postpone everything. Contractors are even partnering up and networking more; one remodeler admitted, “I am very worried… now looking at a very possible recession,” and he began reaching out to other home renovation companies to team up on projects and keep work coming. In short, there’s a hustle mentality – finding creative ways to drum up business – that becomes more prevalent when the economy softens.

Pricing trends have likewise shifted. In recent years, inflation drove up the costs of materials and labor, forcing many service pros to raise their rates. (For instance, a landscaper in Minnesota noted he had to hike his lawn-mowing fee from $50 to $62.50 due to higher fuel and wage costs.) Now, with inflation easing and demand not as red-hot, contractors can’t keep raising prices without losing customers. Recent industry data shows that by late 2024, some segments (like plumbing, HVAC, electrical contracting ) saw fewer new jobs being booked , yet median revenue for those businesses held steady – which implies many providers maintained income by charging a bit more per job or focusing on higher-value projects. Essentially, they’re doing slightly fewer jobs but not experiencing a revenue freefall, thanks to careful pricing adjustments. At the same time, there’s anecdotal evidence of discounting and deals to spur hesitant customers: home improvement marketing advisors recommend offering “limited-time promotions” or bonus upgrades (e.g. free fixture upgrades or design consultations) during slow periods to nudge homeowners into action. Some builders will even temporarily trim their profit margins – accepting lower profit per project just to keep crews busy – because earning a smaller profit is better than having no work at all. This kind of bargain offer was virtually nonexistent at the height of the boom, but it becomes a viable strategy in a slowdown. On the availability side, homeowners today are finding it easier to line up contractors for projects compared to the peak pandemic years. The frantic backlog of 2021 has eased: as noted, many pros now have openings within weeks rather than months. However, it’s worth noting that skilled labor is still in short supply in many trades, which puts a floor under how “loose” the market can get. Even as demand cooled, the construction industry hasn’t magically gained a glut of plumbers or electricians – there remains a long-term shortage of qualified tradespeople. In fact, a late-2024 Angi survey found 54% of homeowners still reported trouble finding qualified professionals , citing delays, higher costs, and limited availability for certain jobs. This paradox is explained by the unique conditions: many contractors left the industry or retired over the past decade, and younger workers aren’t filling all those gaps. So while you might see more ads for a “cheap plumber” or off-season discounts now than two years ago, it doesn’t mean contractors are sitting idle en masse – it simply means the balance of power has shifted slightly back toward consumers . Compared to 2021’s frenzy, homeowners have a bit more leverage (and can shop around for deals), but top-notch pros in certain specialties may still be booked out due to the structural labor shortage.

Regional Variations in Home Service Demand

If the U.S. economy is cooling, where is it “worse” or “better” in terms of home services? The impact isn’t uniform across all regions – local economic factors and housing dynamics play a big role. Recent data on home improvement spending reveals that some parts of the country are still seeing robust activity , while others have pulled back more sharply, creating differences in how hard plumbers and other pros are chasing work. According to an analysis of home improvement loan statistics, the Mountain West and New England regions have remained relatively strong for renovation spending. In 2023, homeowners in Utah and Idaho took out the most home improvement loans per capita – about 17.0 and 13.0 loans per 1,000 homeowners, respectively, topping the nation. Other high-ranking states included Oregon, Colorado, Washington , and several in the Northeast like Rhode Island, New Hampshire, Vermont, and Massachusetts. These locations are a mix of fast-growing areas and places with older housing stock, both of which can drive renovation demand. The data suggests that despite the overall slowdown, many households in those states continued investing in their homes – perhaps due to strong local economies or the necessity of upgrading aging homes. For example, the Salt Lake City metro in Utah ranked #1 among large metropolitan areas for home improvement loan activity in 2023. Even Charlotte, NC – which saw a cooling from its peak – ranked among the top 10 large metros for home improvement investment that year, indicating that some level of demand persisted in such markets. By contrast, several regions – particularly parts of the South – saw much lower home improvement activity, implying a tougher climate for home contractors. At the state level, Louisiana was dead last in 2023 (only ~2.1 loans per 1,000 homeowners), and the data shows major Texas cities were also near the bottom. In fact, San Antonio and Houston had just ~2.4–2.6 home improvement loans per 1,000 homeowners, and the Dallas-Fort Worth area about 4.1 per 1,000 – all well below the national average. These low figures suggest that in much of Texas (despite a growing population), homeowners were holding off on renovation projects more than elsewhere. This could be due to economic reasons (e.g. sensitivity to higher interest rates or less equity to tap), or simply because many homes in rapidly built Sun Belt suburbs are relatively newer and don’t yet need large-scale repairs. Regardless, the outcome is that contractors in those markets likely felt a sharper drop in demand , with more competition for the few jobs that homeowners were green-lighting. Similarly, some big coastal markets like New York or the Bay Area also showed low per-capita home improvement loan activity in 2023, possibly reflecting high costs and economic uncertainty causing a pause on remodeling there as well. In summary, the “plumbers and handymen offering deals” phenomenon as an economic sign can be observed unevenly: It’s more evident in areas that have seen the steepest slowdowns in home improvement spending, and less so in pockets that remain busy. Fast-growing Western states and parts of New England still had considerable home upgrade activity (so pros there may be staying busy without heavy discounting), whereas many parts of the South and some expensive coastal cities saw homeowners hit the brakes, leaving contractors scrambling for work. This aligns with the notion that during lean times, home service professionals become more eager for business – they shorten wait times, advertise discounts, and broaden their services – especially in the locales where the economic pinch is felt hardest.

Conclusion

While the United States is not in an official recession as of early 2025, the housing and home improvement sector has gone through a noticeable slowdown. High interest rates and inflation have made consumers cautious, leading to fewer big remodeling jobs and more deferred maintenance. In response, plumbers, electricians, remodelers and other home service pros are indeed hustling more for work . We see it in pricing (fewer rapid hikes, more special offers), in availability (contractors actually returning calls and fitting you in sooner), and in advertising (seasonal deals, “buy now” promotions, networking for referrals). One remodeling marketer described 2024 as “one of the slowest years in terms of lead generation since [the] 2020 [boom]” , underscoring how much the landscape has changed. The good news is that this dip is broadly expected to be temporary – forecasts predict a rebound in home improvement spending by mid-2025, especially as interest rates ease. For now, though, those telltale signs are visible: in many U.S. neighborhoods, the home pros are knocking a bit harder . They’re offering that extra discount or free estimate , and they’re eager to secure your business – a classic sign that the economy, while not collapsed, is running cooler than in the recent past. Homeowners can take advantage of this environment to negotiate good deals, but should also plan projects carefully (focusing on needed repairs and value-adding improvements) until confidence and budgets fully recover. The “plumber index” may be an informal gauge, but it does reflect real trends: right now, it’s indicating a period of softened demand where service providers are working harder to win jobs, consistent with a mildly recessionary climate in the home services arena.

Sources:

- Harvard Joint Center for Housing Studies & Construction Coverage – Home improvement spending trends and regional loan data constructioncoverage.com constructioncoverage.com .

- Angi 2024 State of Home Spending – Home project spending dropped 12% in 2024; 93% still plan projects for 2025 nasdaq.com nasdaq.com .

- Builder Funnel (Camille Henderson) – 2024 saw slowest remodeling leads since 2020; advice to offer promotions and cut margins during slowdowns info.builderfunnel.com info.builderfunnel.com .

- AP News (via CBS/LA Times) – Contractors report shorter backlogs, more cost-conscious customers as housing market cooled (examples from NC, MA in 2022–23) cbsnews.com cbsnews.com .

- Jobber Q3 2024 Home Service Report – Home services had a slower first half of 2024, then regained momentum; contracting segment saw fewer jobs but steady revenue via higher-value work prnewswire.com prnewswire.com .

- Home Improvement Research Institute (HIRI) – Economists expect no official recession in 2025 but continued below-trend growth hiri.org .

- Farnsworth Group & others – Plumbing industry faced slight decline in 2023; persistent labor shortages in trades thefarnsworthgroup.com thefarnsworthgroup.com .